By Justin Cope, justin.cope@house.mn

Economic Development

Property Tax Abatement

January 2023

What is economic development property tax abatement?

Minnesota law allows political subdivisions—cities, counties, school districts, and towns—to abate

property taxes in order to promote local economic growth. Minn. Stat. §§ 469.1812-469.1815. Economic

development property tax abatements differ from traditional abatements where the valuation of the

property, its property taxes, or its costs, interest, or penalties of property taxation are reduced. An

economic development abatement allows a political subdivision to expend money to benefit a property

in one of a number of ways, including by reducing property taxes, deferring payment of property taxes,

or spending the money directly on improving the property. A political subdivision will often grant an

abatement pursuant to an abatement agreement with the landowner; in exchange for the abatement,

the land owner agrees to develop the land in a way that will promote local economic development.

When and how can an economic development abatement be granted?

To grant an abatement, the political subdivision must expect the benefits of the abatement to equal or

exceed its costs. The political subdivision must also find that the abatement will serve the public good in

one of a number of ways, such as increasing the tax base, redeveloping blighted areas, or providing

employment opportunities, public facilities, or access to services.

Before granting an abatement, a political subdivision must provide notice of the prospective abatement

and hold a public hearing. After the hearing, the governing body of the political subdivision may grant an

abatement by adopting an abatement resolution that specifies the terms of the abatement.

Which property taxes may be abated?

A political subdivision may only abate the property taxes it imposes by resolution. It cannot abate the

taxes imposed by another political subdivision, by the state, or by a special taxing district, such as a

watershed district. It also cannot abate taxes imposed pursuant to state law, such as the fiscal disparities

tax. Despite these limitations, a political subdivision may grant an economic development abatement at

an amount that offsets one of these taxes.

What are the limits on an abatement?

Usually, an abatement can last no more than 15 years, but a political subdivision may extend the

duration to 20 years if it asks the other political subdivisions containing the property to grant the

property an abatement and if any of the other political subdivisions refuses the request.

When adopting the abatement resolution, the political subdivision may limit the abatement to a specific

dollar amount per year or in total, to increases in property taxes resulting from increases in property

value, or to interest and penalties if it chooses to grant the abatement as a deferral of property tax

payments by the parcel owner. The annual value of all economic development abatements granted by a

political subdivision may not exceed the greater of (1) $200,000, or (2) 10 percent of the net tax capacity

of the political subdivision.

Economic Development Property Tax Abatement

How is an abatement implemented?

An abatement may take several forms: the political subdivision may pay the parcel owner the amount of

the abatement; the political subdivision may defer payment of property taxes on the parcel and forgive

interest and penalties for late payment; or the political subdivision may use the money directly to

improve public infrastructure. No matter how the political subdivision implements the abatement, the

amount of the abatement is added to the subdivision’s property tax levy, which is collected through

taxation on all properties in the subdivision, including the parcel receiving the abatement.

What bonding powers does a political subdivision granting an abatement

have?

A political subdivision granting an economic development abatement may issue bonds to be paid with

the abatement. The bonds can be general obligation bonds or revenue bonds and can be used for a

number of purposes, including paying for public improvements, acquiring land, or reimbursing the

property owner for improvements to the land. The Department of Education advises school districts that

without voter approval, they may only issue abatement bonds for school parking improvements.

1

How do abatements compare with tax increment financing?

The legislature designed the abatement law as an alternative to and a supplement to tax increment

financing (TIF). Both tools can be used for similar purposes, rely on property tax funding, and have

similar bonding powers, but they differ in at least three important respects. First, some TIF districts last

25 years, while abatements typically last only 15 years. Second, TIF allows a municipality acting

unilaterally to capture all local property taxes, while an abatement captures only the property taxes

imposed by the granting political subdivision. Finally, TIF is subject to more legal restrictions than an

abatement. Restrictions on TIF include a blight test for redevelopment districts, the but-for test, and

strict limits on how increments may be spent. (See the House Research website for more information on

TIF at www.house.mn/hrd/issinfo/tifmain.aspx.)

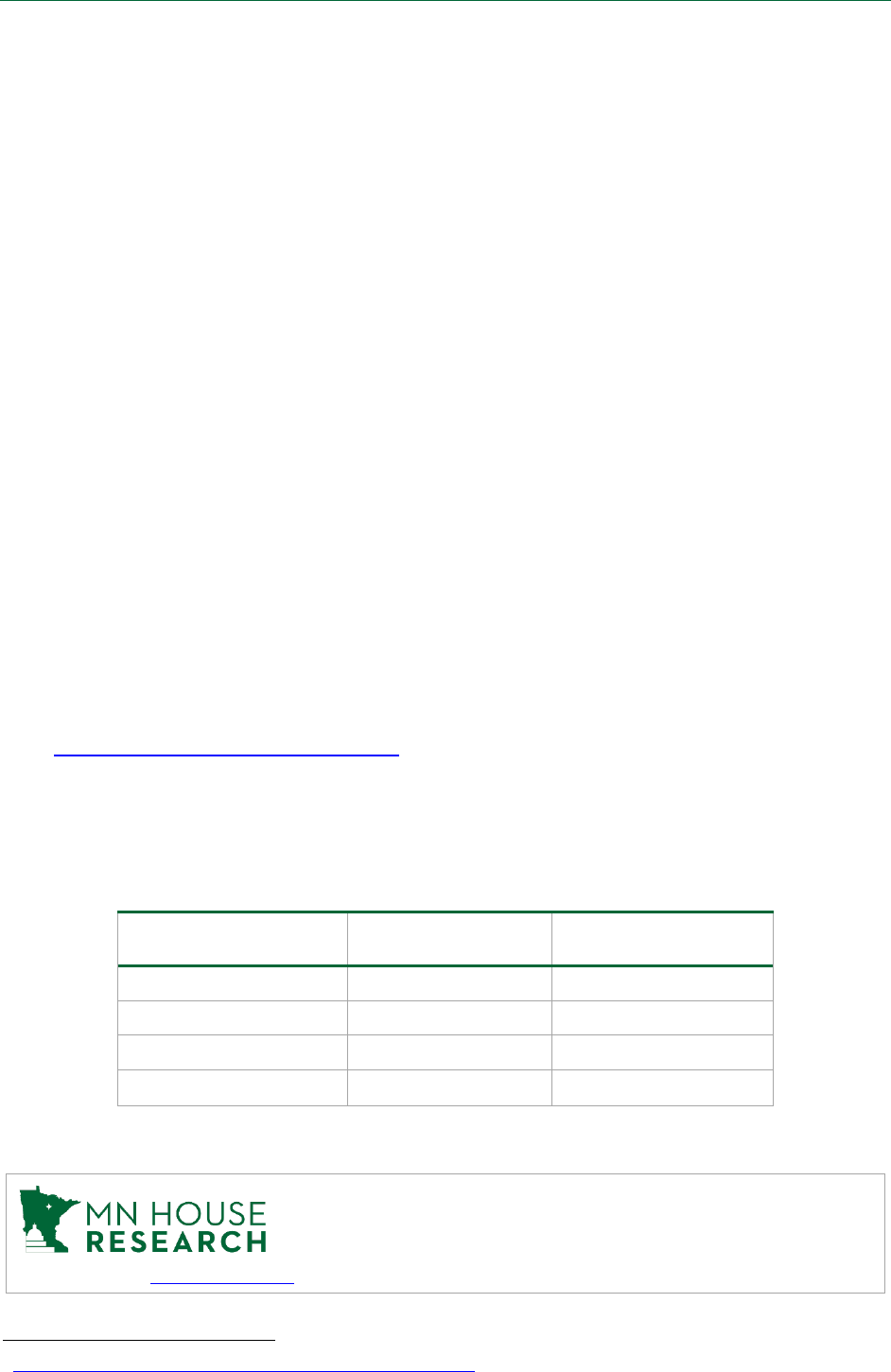

How widely has abatement been used?

The following amounts of abatement levies were reported for property taxes payable in 2022, as

reported to the Departments of Revenue (cities and counties) and Education (schools).

Political Subdivision Number Amount

Cities 70 $13,052,859

Counties 40 $2,517,907

School districts 11 $347,000

Total 121 $15,917,766

Minnesota House Research Department provides nonpartisan legislative, legal, and

information services to the Minnesota House of Representatives. This document

can be made available in alternative formats.

www.house.mn./hrd | 651-296-6753 | 155 State Office Building | St. Paul, MN 55155

1

https://education.mn.gov/MDE/dse/schfin/fac/MDE073628