Statement on October 2021

Auditing Standards 145

Issued by the Auditing Standards Board

Understanding the Entity and Its Environment and

Assessing the Risks of Material Misstatement

(Supersedes Statement on Auditing Standards (SAS) No. 122, Statements on Auditing Standards:

Clarification and Recodification, as amended, section 315, Understanding the Entity and Its

Environment and Assessing the Risks of Material Misstatement [AICPA, Professional

Standards, AU-C sec. 315]; Amends

• SAS No. 122, as amended

— Section 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit

in Accordance With Generally Accepted Auditing Standards [AICPA, Professional

Standards, AU-C sec. 200]

— Section 210, Terms of Engagement [AICPA, Professional Standards, AU-C sec. 210]

— Section 230, Audit Documentation [AICPA, Professional Standards, AU-C sec. 230]

— Section 240, Consideration of Fraud in a Financial Statement Audit [AICPA, Professional

Standards, AU-C sec. 240]

— Section 250, Consideration of Laws and Regulations in an Audit of Financial Statements

[AICPA, Professional Standards, AU-C sec. 250]

— Section 260, The Auditor’s Communication With Those Charged With Governance

[AICPA, Professional Standards, AU-C sec. 260]

— Section 265, Communicating Internal Control Related Matters Identified in an Audit

[AICPA, Professional Standards, AU-C sec. 265]

— Section 300, Planning an Audit [AICPA, Professional Standards, AU-C sec. 300]

— Section 330, Performing Audit Procedures in Response to Assessed Risks and Evaluating

the Audit Evidence [AICPA, Professional Standards, AU-C sec. 330]

— Section 402, Audit Considerations Relating to an Entity Using a Service Organization

[AICPA, Professional Standards, AU-C sec. 402]

— Section 501, Audit Evidence — Specific Considerations for Selected Items [AICPA,

Professional Standards, AU-C sec. 501]

— Section 505, External Confirmations [AICPA, Professional Standards, AU-C sec. 505]

— Section 530, Audit Sampling [AICPA, Professional Standards, AU-C sec. 530]

— Section 550, Related Parties [AICPA, Professional Standards, AU-C sec. 550]

— Section 600, Special Considerations — Audits of Group Financial Statements (Including

the Work of Component Auditors) [AICPA, Professional Standards, AU-C sec. 600]

— Section 620, Using the Work of an Auditor’s Specialist [AICPA, Professional Standards,

AU-C sec. 620]

— Section 805, Special Considerations — Audits of Single Financial Statements and Specific

Elements, Accounts, or Items of a Financial Statement [AICPA, Professional Standards,

AU-C sec. 805]

— Section 930, Interim Financial Information [AICPA, Professional Standards, AU-C sec.

930]

• SAS No. 128, Using the Work of Internal Auditors [AICPA, Professional Standards, AU-C sec.

610]

• SAS No. 130, An Audit of Internal Control Over Financial Reporting That Is Integrated With

an Audit of Financial Statements, as amended [AICPA, Professional Standards, AU-C sec.

940]

• SAS No. 134, Auditor Reporting and Amendments, Including Amendments Addressing

Disclosures in the Audit of Financial Statements, as amended

— Section 701, Communicating Key Audit Matters in the Independent Auditor’s Report

[AICPA, Professional Standards, AU-C sec. 701]

• SAS No. 136, Forming an Opinion and Reporting on Financial Statements of Employee

Benefit Plans Subject to ERISA, as amended [AICPA, Professional Standards, AU-C sec. 703]

• SAS No. 137, The Auditor’s Responsibilities Relating to Other Information Included in

Annual Reports, as amended [AICPA, Professional Standards, AU-C sec. 720]

• SAS No. 142, Audit Evidence [AICPA, Professional Standards, AU-C sec. 500]

• SAS No. 143, Auditing Accounting Estimates and Related Disclosures, as amended [AICPA,

Professional Standards, AU-C sec. 540])

© 2021 American Institute of Certified Public Accountants, Inc. All rights reserved.

For information about the procedure for requesting permission to make copies of any part of this work,

please email copyright-permissions@aicpa-cima.com with your request. Otherwise, requests should be

written and mailed to Permissions Department, 220 Leigh Farm Road, Durham, NC 27707-8110.

Statement on Auditing Standards, Understanding the Entity and Its

Environment and Assessing the Risks of Material Misstatement

Executive Summary

Overview

The Auditing Standards Board (ASB) has issued Statement on Auditing Standards (SAS) No. 145,

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, to

supersede SAS No. 122, as amended, section 315 of the same title, and to amend various AU-C

sections in AICPA Professional Standards. SAS No. 145, for example, enhances the following:

• Requirements and guidance related to the auditor’s risk assessment, in particular,

obtaining an understanding of the entity’s system of internal control and assessing

control risk

• Guidance that addresses the economic, technological, and regulatory aspects of the

markets and environment in which entities and audit firms operate

SAS No. 145 also includes, among other things, the following:

• Revised requirements to evaluate the design of certain controls within the control

activities component, including general IT controls, and to determine whether such

controls have been implemented

• New requirement to separately assess inherent risk and control risk

• New requirement to assess control risk at the maximum level such that, if the auditor

does not plan to test the operating effectiveness of controls, the assessment of the risk of

material misstatement is the same as the assessment of inherent risk

• A revised definition of significant risk

• New guidance on scalability

• New guidance on maintaining professional skepticism

• A new “stand-back” requirement intended to drive an evaluation of the completeness

of the auditor’s identification of significant classes of transactions, account balances, and

disclosures

• Revised requirements relating to audit documentation

• A conforming amendment to perform substantive procedures for each relevant assertion of

each significant class of transactions, account balance, and disclosure, regardless of the

assessed level of control risk (rather than for all relevant assertions related to each

material class of transactions, account balance, and disclosure, irrespective of the assessed

risks of material misstatement, as previously required).

SAS No. 145 does not fundamentally change the key concepts underpinning audit risk, which is a

function of the risks of material misstatement and detection risk. Rather, SAS No. 145 clarifies and

enhances certain aspects of the identification and assessment of the risks of material misstatement to

drive better risk assessments and, therefore, enhance audit quality.

The SAS becomes effective for audits of financial statements for periods ending on or after

December 15, 2023.

Introduction

This executive summary provides an overview of SAS No. 145. This document aims to highlight

changes that are viewed to be of most interest (but is not inclusive of all changes).

Background

Deficiencies in the auditor’s risk assessment procedures is a common issue identified by practice

monitoring programs in the United States and worldwide. In 2020 U.S. peer reviews, AU-C section

315 was the leading source of matters for further consideration (MFCs), constituting 25 percent of

MFCs.

1

The ASB’s project to enhance the auditing standards relating to the auditor’s risk assessment through

the issuance of SAS No. 145 was intended to enable auditors to appropriately address the following:

a. Understanding the entity’s system of internal control, in particular, relating to the

auditor’s work effort to obtain the necessary understanding

b. Modernizing the standard in relation to IT considerations, including addressing risks

arising from an entity’s use of IT

c. Determining risks of material misstatement, including significant risks

Convergence

The ASB has a strategic objective to converge with the International Standards on Auditing (ISAs).

Accordingly, SAS No. 145 was developed using ISA 315, Identifying and Assessing the Risks of

Material Misstatement (Revised 2019), as the base starting point. ISA 315 (Revised 2019) is

effective for audits of financial statements for periods beginning on or after December 15, 2021.

As part of the convergence efforts, it is intended that the requirements in each SAS differ from its

corresponding ISA only where the ASB believes compelling reasons exist for the differences. AU-C

Appendix B, “Substantive Differences Between the International Standards on Auditing and

Generally Accepted Auditing Standards,” of AICPA Professional Standards includes an analysis

1

AICPA Center for Plain English Accounting, Improving Risk Assessments in Private Company Audits, July 21, 2021,

https://www.aicpa.org/interestareas/centerforplainenglishaccounting.html.

prepared by the AICPA Audit and Attest Standards staff that highlights substantive differences

between the requirements of the SASs and ISAs, and the rationales therefor.

Link to SAS No. 143, Auditing Accounting Estimates and Related Disclosures

Some of the new concepts in SAS No. 145 have already been introduced into generally accepted

auditing standards (GAAS) in SAS No. 143, Auditing Accounting Estimates and Related Disclosures,

including inherent risk factors, the spectrum of inherent risk, and the separate assessments of inherent

risk and control risk. These concepts are applicable to all types of classes of transactions, account

balances, and disclosures, not just those involving accounting estimates. Because of the close

interaction between SAS No. 145 and SAS No. 143, their effective dates have been aligned such that

both standards will be effective for audits of financial statements for periods ending on or after

December 15, 2023.

Fundamental Aspects of SAS No. 145

SAS No. 145 builds on the foundational concepts relating to an audit of financial statements in AU-

C section 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in

Accordance With Generally Accepted Auditing Standards, (such as audit risk, identifying risks at

the financial statement and assertion levels, and the definitions of inherent risk and control risk).

SAS No. 145 is principles based and audit methodology–neutral. The degree to which SAS No. 145

might affect an audit methodology may vary based on the particular audit approach and related audit

methods, tools, or techniques.

Scalability of SAS No. 145 [Enhanced and New Guidance]

Complexity of an entity’s activities and its environment, including its system of internal control, is

the primary driver of scalability in the application of SAS No. 145. SAS No. 145 has removed the

“Considerations Specific to Smaller Entities” sections previously included in the application material

but has incorporated most of that content elsewhere in the standard, as appropriate, together with

further revisions to promote scalability. SAS No. 145 recognizes that, although the size of an entity

may be an indicator of its complexity, some smaller entities may be complex, and some larger

entities may be less complex.

In addition, SAS No. 145 recognizes that some aspects of the entity’s system of internal control may

be less formalized but still present and functioning, considering the nature and complexity of the

entity. When the entity’s systems and processes lack formality, the auditor may still be able to

perform risk assessment procedures through a combination of inquiries and other risk assessment

procedures (for example, corroborating inquiries about the entity’s processes through observation or

inspection of documents).

Maintaining Professional Skepticism [Enhanced and New Guidance]

SAS No. 145 contains several key provisions that are designed to enhance and emphasize the

auditor’s professional skepticism, including the following:

• Clarifying that an appropriate understanding of the entity and its environment, and the

applicable financial reporting framework, provides a foundation for being able to

maintain professional skepticism throughout the audit

• Highlighting the benefits of maintaining professional skepticism during the required

engagement team discussion

• Highlighting that contradictory evidence may be obtained as part of the auditor’s risk

assessment procedures.

Modernization for an Evolving Business Environment [New Guidance]

SAS No. 145 includes additional guidance that addresses significant changes in, and the evolution

and increasingly complex nature of, the economic, technological, and regulatory aspects of the

markets and environment in which entities and audit firms operate. It also recognizes the ability to

use automated tools and techniques (including audit data analytics) when performing risk assessment

procedures.

Obtaining an Understanding of the Entity and Its Environment, and the Applicable Financial

Reporting Framework (Paragraphs 19−20) [New Requirements]

SAS No. 145 elevates the importance of understanding the applicable financial reporting framework

by restructuring the previous requirements. In addition, SAS No. 145 includes the following:

• A new explicit requirement to understand the use of IT in the entity’s structure,

ownership and governance, and business model. SAS No. 145 defines the IT

environment, which includes IT applications and supporting IT infrastructure, as well as

the IT processes and personnel involved in those processes, that an entity uses to

support business operations and achieve business strategies.

• A new requirement to obtain an understanding of how inherent risk factors affect

susceptibility of assertions to misstatement and the degree to which they do so, in the

preparation of the financial statements in accordance with the applicable financial reporting

framework (the concept of inherent risk factors is described further in the text that

follows).

Obtaining an Understanding of the Entity’s System of Internal Control (Paragraphs 21−31)

[New Requirements and Enhanced Guidance]

Understanding certain aspects of the entity’s system of internal control is integral to the auditor’s

identification and assessment of the risks of material misstatement, regardless of the auditor’s

planned controls reliance strategy. SAS No. 145 clarifies that the overall understanding of the entity’s

system of internal control is achieved through understanding, and evaluating certain aspects of, each

of the following components of the system of internal control (and performing the related

requirements to obtain such an understanding):

1. The control environment

2. The entity’s risk assessment process

3. The entity’s process to monitor the system of internal control

4. The information system and communication

5. Control activities

Each component comprises a collection of controls, which may be direct or indirect.

2

Although

differing requirements exist with respect to each component, SAS No. 145 clarifies the auditor’s

responsibilities, including the requirements to evaluate the design of certain controls within the

control activities component and determine whether such controls have been implemented.

The nature, timing, and extent of risk assessment procedures that the auditor performs to obtain the

required understanding are 1) matters of the auditor’s professional judgment, and 2) based on the

auditor’s determination of the procedures that will provide sufficient appropriate audit evidence to

serve as a basis for the identification and assessment of the risks of material misstatement.

Terms Used to Describe Aspects of the Entity’s System of Internal Control

SAS No. 145 applies certain revised terms consistently. These changes, made throughout GAAS,

include the following:

• The term internal control has been changed to system of internal control, and the definition

has been updated to reflect that it comprises five interrelated components.

• The use of the term controls has been clarified by including the following definition in the

standard: (see paragraph 12)

“Policies or procedures that an entity establishes to achieve the control objectives of

management or those charged with governance. In this context

i. policies are statements of what should, or should not, be done within the entity to

effect control. Such statements may be documented, explicitly stated in

communications, or implied through actions and decisions.

ii. procedures are actions to implement policies.”

Understanding the Components of the Entity’s System of Internal Control

When identifying controls that address the risks of material misstatement, SAS No. 145 clarifies

the requirement to evaluate the design and determine the implementation of certain controls

within the control activities component. These controls include the following:

2

Direct controls are controls that are precise enough to address risks of material misstatement at the assertion level.

Indirect controls are controls that support direct controls. Although indirect controls are not sufficiently precise to

prevent, or detect and correct, misstatements at the assertion level, they are foundational and may have an indirect

effect on the likelihood that a misstatement will be prevented or detected on a timely basis.

• Controls that address a risk that is determined to be a significant risk

• Controls over journal entries and other adjustments as required by AU-C section 240,

Consideration of Fraud in a Financial Statement Audit

• Controls for which the auditor plans to test operating effectiveness in determining the

nature, timing, and extent of substantive procedures, which includes controls that address

risks for which substantive procedures alone do not provide sufficient appropriate audit

evidence

• Other controls that, based on the auditor’s professional judgment, the auditor considers

appropriate to enable the auditor to assess the risks of material misstatement at the

assertion level and to design further audit procedures

As described further in the text that follows, SAS No. 145 also requires the auditor to identify general

IT controls that address the risks arising from the use of IT and to evaluate their design and determine

their implementation.

The controls for which the auditor is required to evaluate design and determine implementation are

referred to as identified controls in SAS No. 145. Such controls might also be referred to as relevant

controls or key controls in some audit methodologies.

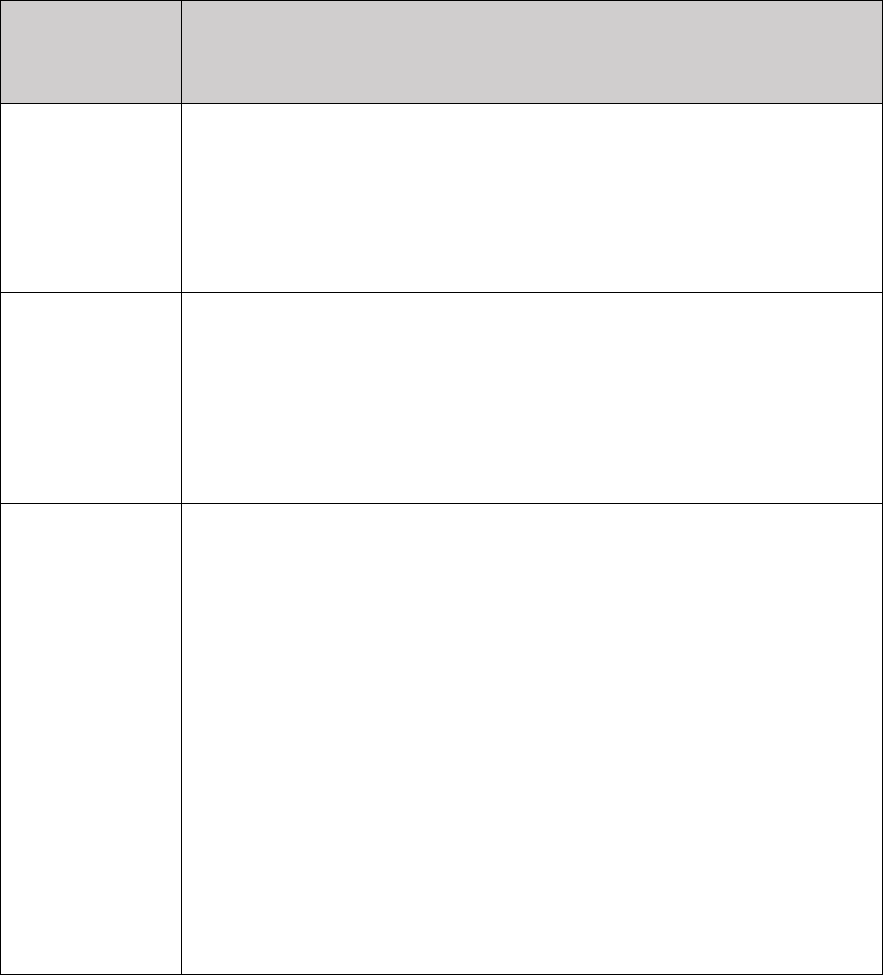

The following table provides a high-level summary of the auditor’s responsibilities and work effort

related to understanding, and evaluating certain aspects of, the components of the entity’s system of

internal control in accordance with SAS No. 145.

Components of the Entity’s System of Internal

Control

Primarily Indirect Controls

Primarily More Direct Controls

but May Be Indirect Controls

Primarily Direct Controls

Control

Environment

Entity’s Risk

Assessment

Process

Entity’s Process to

Monitor the System

of Internal Control

Information System and

Communication

Control Activities

SAS No. 145 includes requirements to understand, and

evaluate certain aspects of, the control environment, the

entity’s risk assessment process, and the entity’s process to

monitor the system of internal control components. The

auditor’s required understanding includes the ongoing tasks

and activities, or processes, geared to the achievement of

the entity’s financial reporting objectives.

Audit evidence for the auditor’s understanding and

evaluation may be obtained through a combination of

inquiries and other risk assessment procedures (for

example, corroborating inquiries about the entity’s

processes through observation or inspection of documents).

The auditor exercises professional judgment to determine

the nature and extent of the procedures to be performed to

the meet the requirements of SAS No. 145.

SAS No. 145 does not require the auditor to evaluate the

design or determine the implementation of individual

controls within these components. However, the auditor

may, based on the auditor’s professional judgment, identify

controls within these components that address risks of

material misstatement at the assertion level for which the

auditor evaluates design and determines implementation.

SAS No. 145 includes a requirement

to understand, and evaluate certain

aspects of, the information system

and communication component. For

this component, the auditor’s

understanding includes, among

other things, the flows of

transactions and other aspects of the

entity’s information-processing

activities for significant classes of

transactions, account balances, and

disclosures as well as the entity’s

communication of significant

matters.

SAS No. 145 does not require the

auditor to evaluate the design or

determine the implementation of

individual controls within the

information and communication

component. It is important to note

that the auditor’s identification and

evaluation of controls in the control

activities component is focused on

information-processing controls,

also known as transaction controls.

SAS No. 145 includes specific requirements to understand certain

controls within the control activities component that address risks of

material misstatement at the assertion level.

For the identified controls that address risks of material misstatement

at the assertion level, the auditor is required to evaluate the design and

determine whether the controls have been implemented. The

identified controls include the following:

•

Controls that address a risk that is determined to be a

significant risk

•

Controls over journal entries and other adjustments as

required by AU-C section 240, Consideration of

Fraud in a Financial Statement Audit

•

Controls for which the auditor plans to test operating

effectiveness in determining the nature, timing, and extent of

substantive procedures, which include controls that address

risks for which substantive procedures alone do not provide

sufficient appropriate audit evidence

•

Other controls that, based on the auditor’s professional

judgment, the auditor considers appropriate to enable the

auditor to assess the risks of material misstatement at the

assertion level and to design further audit procedures.

Identified controls also include those general IT controls that address

risks arising from the use of IT, as described in the following section.

Risks Arising From the Use of IT and General IT Controls

SAS No. 145 now defines the terms risks arising from the use of IT and general IT controls. SAS

No. 145 requires the auditor to identify general IT controls that address the risks arising from the

use of IT and to evaluate their design and determine their implementation.

General IT controls need not be identified for every IT process. General IT controls are identified

based on the risks arising from the use of IT. To identify the risks arising from the use of IT, the

auditor identifies the IT applications and other aspects of the entity’s IT environment that are

subject to such risks. Such IT applications and other aspects are identified based on the identified

controls that address the risks of material misstatement at the assertion level, as described in the

preceding table under “control activities.” Appendix E, “Considerations for Understanding IT,”

of SAS No. 145 includes guidance that may be relevant in identifying IT applications and other

aspects of the IT environment that may be subject to risks arising from the use of IT.

Other Matters Relevant to Understanding the Entity’s System of Internal Control

Consistent with AU-C section 265, Communicating Internal Control Related Matters Identified

in an Audit, SAS No. 145 includes an explicit requirement that, based on the auditor’s

understanding, and evaluation of certain aspects of, the components of the entity’s system of

internal control as required by SAS No. 145, the auditor should determine whether one or more

control deficiencies have been identified. The auditor may determine that a significant deficiency

or material weakness exists that affects the auditor’s risk assessments and related response.

Identifying and Assessing the Risks of Material Misstatement (Paragraphs 32−38) [New

Requirements and Enhanced Guidance]

The auditor’s risk identification and assessment process is iterative and dynamic. In obtaining the

understanding required by SAS No. 145, initial expectations of risks may be developed, which

may be further refined as the auditor progresses through the risk identification and assessment

process.

To assist auditors in understanding the requirements related to the identification and assessment

of the risks of material misstatement, SAS No. 145 clarifies various requirements and also

introduces new concepts and definitions, as described in the following table.

Inherent risk

factors and

spectrum of

inherent risk

(new)

Inherent risk factors are characteristics of events or conditions that affect the

susceptibility to misstatement, whether due to fraud or error, of an assertion about

a class of transactions, account balance, or disclosure, before consideration of

controls. Such factors may be quantitative or qualitative and include complexity,

subjectivity, change, uncertainty, and susceptibility to misstatement due to

management bias or other fraud risk factors insofar as they affect inherent risk.

Depending on the degree to which the inherent risk factors affect the susceptibility

of an assertion to misstatement, the level of inherent risk varies on a scale that is

referred to as the spectrum of inherent risk. The spectrum of inherent risk provides

a frame of reference in determining the significance of the combination of the

likelihood and magnitude of a misstatement.

Inherent risk factors are intended to assist the auditor in focusing on those aspects

of events or conditions that affect an assertion’s susceptibility to misstatement,

which, in turn, facilitates a more focused identification of risks of material

misstatement at the assertion level. Understanding the degree to which inherent risk

factors affect susceptibility of assertions to misstatement assists the auditor in

assessing inherent risk, which also informs the auditor’s design of further audit

procedures in accordance with AU-C section 330, Performing Audit Procedures in

Response to Assessed Risks and Evaluating the Audit Evidence Obtained. It is the

intersection of the magnitude and likelihood of the material misstatement on the

spectrum of inherent risk that will determine whether the assessed inherent risk is

higher or lower on the spectrum of inherent risk.

Relevant

assertions

(revised)

The definition of a relevant assertion was revised to clarify that an assertion

about a class of transactions, account balance, or disclosure is relevant when it

has an identified risk of material misstatement, taking into account the likelihood

and magnitude of a misstatement. A risk of material misstatement exists when (a)

there is a reasonable possibility of a misstatement occurring (that is, its

likelihood), and (b) if it were to occur, there is a reasonable possibility of the

misstatement being material (that is, its magnitude).

SAS No. 145 also clarifies that there is a reasonable possibility when the likelihood

of a material misstatement occurring is more than remote. This guidance is

consistent with that provided in other AU-C sections (for example, AU-C section

265).

The determination of whether an assertion is a relevant assertion continues to be

made before consideration of any related controls (that is, the determination is

based on inherent risk).

Significant

class of

transactions,

account

balance, or

disclosure

(new)

Although the term significant class of transactions, account balance, or disclosure

is used within GAAS, particularly within AU-C section 940, An Audit of Internal

Control Over Financial Reporting That Is Integrated With an Audit of Financial

Statements, it was not defined. A class of transactions, account balance, or

disclosure is considered significant when it has an identified risk of material

misstatement at the assertion level (that is, there is one or more relevant assertions

as defined in the previous section of this table). The determination of whether a

class of transactions, account balance, or disclosure is significant is made before

consideration of any related controls (that is, the determination is based on inherent

risk). The definition and guidance in SAS No. 145 are consistent with how the term

was interpreted by various auditors when applying AU-C section 940.

The introduction of the concept of a significant class of transactions, account

balance, or disclosure is intended to clarify the scope of the auditor’s understanding

of the entity’s information-processing activities as well as the auditor’s

responsibilities related to the identification and assessment of, and responses to,

risks of material misstatement.

As a reminder, AU-C section 240 continues to address the auditor’s responsibilities relating to

fraud in an audit of financial statements and expands on how SAS No. 145 and AU-C section

330 are to be applied regarding risks of material misstatement due to fraud.

Assessing Inherent Risk and Control Risk Separately

For risks of material misstatement at the assertion level, SAS No. 145 now requires separate

assessments of inherent risk and control risk, which is consistent with SAS No. 143, Auditing

Accounting Estimates and Related Disclosures.

SAS No. 145, however, does not prescribe a

specific method for making such risk assessments nor does it require a combined assessment of

inherent risk and control risk. The auditor’s separate assessments of inherent risk and control risk

may be performed in different ways, depending on preferred audit techniques or methodologies,

and may be expressed in different ways.

Assessing Control Risk at the Maximum Level

If the auditor does not plan to test the operating effectiveness of controls, SAS No. 145 now

requires the auditor to assess control risk at the maximum level such that the assessment of the

risk of material misstatement is the same as the assessment of inherent risk. In other words, tests

of the operating effectiveness of controls are required to support a control risk assessment below

the maximum level.

When the auditor does not plan to test the operating effectiveness of identified controls, the

auditor’s evaluation of the design and determination of the implementation of controls may still

assist in the design of substantive procedures. When identified controls are designed effectively

and implemented, risk assessment procedures may influence the auditor’s determination of the

nature and timing of substantive procedures to be performed (for example, the auditor may

determine to perform inspection, rather than external confirmation, or to perform procedures at

an interim date, rather than at period end).

Significant Risks

To promote a more consistent approach to determining significant risks, SAS No. 145 revised the

definition of significant risks to focus not on the response (that is, whether a risk requires special

audit consideration), as was the case with the previous definition, but on the inherent risk

assessment. Accordingly, the definition in SAS No. 145 focuses on those risks for which the

assessment of inherent risk is close to the upper end of the spectrum of inherent risk due to the

degree to which inherent risk factors affect the combination of the likelihood of a misstatement

occurring and the magnitude of the potential misstatement should that misstatement occur.

Significant risks also include those that are to be treated as a significant risk in accordance with

the requirements of other AU-C sections (that is, AU-C section 240 and AU-C section 550,

Related Parties).

SAS No. 145 no longer requires the auditor to determine whether a financial statement level risk

is a significant risk. However, identified risks of material misstatement at the financial statement

level may affect the auditor’s assessment of significant risks at the assertion level.

SAS No. 145 acknowledges that the determination of whether a risk is a significant risk requires

the exercise of professional judgment. AU-C section 330 continues to include special audit

considerations in the form of specific requirements related to significant risks because of the

nature of the risk and the likelihood and potential magnitude of misstatement related to the risk.

Classes of Transactions, Account Balances, and Disclosures That Are Not Significant but

Are Material (Paragraph 40) [New and Revised Requirements]

SAS No. 145 includes a new “stand-back” requirement intended to drive an evaluation of the

completeness of the identification of significant classes of transactions, account balances, and

disclosures by the auditor. For material classes of transactions, account balances, or disclosures

that have not been determined to be significant classes of transactions, account balances, or

disclosures (that is, there are no relevant assertions identified), SAS No. 145 requires the auditor

to evaluate whether the auditor’s determination remains appropriate. Materiality is in the context

of the financial statements. Accordingly, classes of transactions, account balances, or disclosures

are material if there is a substantial likelihood that omitting, misstating, or obscuring information

about them would influence the judgment made by a reasonable user based on the financial

statements.

The stand-back differs from the requirement in paragraph .18 of AU-C section 330, which was

revised to align with the definitions in SAS No. 145 and with PCAOB AS 2301, The Auditor's

Responses to the Risks of Material Misstatement. Paragraph .18 of AU-C section 330 now

requires the auditor to perform substantive procedures for each relevant assertion of each

significant class of transactions, account balance, and disclosure, regardless of the assessed level

of control risk (rather than for all relevant assertions related to each material class of

transactions, account balance, and disclosure, irrespective of the assessed risks of material

misstatement, as previously required) [emphasis added].

Audit Documentation (Paragraph 42) [New Requirements]

SAS No. 145 also revises the audit documentation requirements to include the following new

requirements:

• Documentation of the evaluation of the design of identified controls and

determination of whether such controls have been implemented

• The rationale for significant judgments made regarding the identified and assessed

risks of material misstatement

The form, content, and extent of audit documentation that is sufficient to enable an experienced

auditor having no previous experience with the audit to understand the nature, timing, and extent

of the risk assessment procedures performed and the results of those procedures, including the

conclusions reached and the rationale for the significant professional judgments made, depend on

various factors, including the need to document a conclusion or the basis for a conclusion

otherwise not readily determinable from the documentation of the work performed or audit

evidence obtained.

Auditing Standards Board

(2021–2022)

Tracy W. Harding, Chair Robert R. Harris

Brad C. Ames Kathleen K. Healy

Maxene M. Bardwell Jon Heath

Patricia Bottomly Clay Huffman

Samantha Bowling J. Gregory Jenkins

Sherry Chesser Maria C. Manasses

Harry Cohen Andrew Prather

Jeanne M. Dee Chris Rogers

Horace Emery Tania DeSilva Sergott

Diane Hardesty

Risk Assessment Task Force

Maria C. Manasses, Chair Susan Jones

Tracy W. Harding, Former Chair April King

Diane Hardesty Tania DeSilva Sergott

Kathleen K. Healy Dan Wernke

AICPA Staff

Jennifer Burns Hiram Hasty

Chief Auditor Associate Director

AICPA Audit and Attest Standards — Public

Accounting

Teighlor S. March

Assistant General Counsel —

Office of General Counsel

Note: Statements on Auditing Standards are issued by the Auditing Standards Board, the senior

technical body of the AICPA designated to issue pronouncements on auditing matters. The

“Compliance With Standards Rule” (ET sec. 1.310.001)

1

of the AICPA Code of Professional

Conduct requires compliance with these standards in an audit of a nonissuer.

1

All ET sections can be found in AICPA Professional Standards.

CONTENTS

Paragraph

Introduction

Scope of This SAS ................................................................................................................... 1

Key Concepts in This SAS .................................................................................................. 2–8

Scalability ................................................................................................................................ 9

Effective Date ........................................................................................................................ 10

Objective ..................................................................................................................................... 11

Definitions ................................................................................................................................... 12

Requirements

Risk Assessment Procedures and Related Activities ....................................................... 13–18

Obtaining an Understanding of the Entity and Its Environment, the Applicable

Financial Reporting Framework, and the Entity’s System of Internal Control ............... 19–31

Identifying and Assessing the Risks of Material Misstatement ....................................... 32–38

Evaluating the Audit Evidence Obtained From the Risk Assessment Procedures ................ 39

Classes of Transactions, Account Balances, and Disclosures That Are Not

Significant but Are Material .................................................................................................. 40

Revision of Risk Assessment ................................................................................................. 41

Documentation ....................................................................................................................... 42

Application and Other Explanatory Material

Definitions.................................................................................................................... A1–A16

Risk Assessment Procedures and Related Activities ................................................. A17–A54

Obtaining an Understanding of the Entity and Its Environment, the Applicable

Financial Reporting Framework, and the Entity’s System of Internal Control ....... A55–A212

Identifying and Assessing the Risks of Material Misstatement ............................. A213–A260

Evaluating the Audit Evidence Obtained From the Risk Assessment Procedures A261–A263

Classes of Transactions, Account Balances, and Disclosures That Are Not

Significant but Are Material .................................................................................. A264–A265

Revision of Risk Assessment ............................................................................................ A266

Documentation ....................................................................................................... A267–A273

Appendix A — Considerations for Understanding the Entity and Its Business

Model ...................................................................................................................................... A274

Appendix B — Understanding Inherent Risk Factors ...................................................... A275

Appendix C — Understanding the Entity’s System of Internal Control ......................... A276

Appendix D — Considerations for Understanding an Entity’s Internal Audit

Function ................................................................................................................................. A277

Appendix E — Considerations for Understanding IT....................................................... A278

Appendix F — Considerations for Understanding General IT Controls ........................ A279

Appendix G — Amendments to Various Statements on Auditing Standards

(SAS), as Amended, and to Various Sections in SAS No. 122, Statements on

Auditing Standards: Clarification and Recodification, as Amended .................................. A280

Statement on Auditing Standards, Understanding the

Entity and Its Environment and Assessing the Risks of

Material Misstatement

Introduction

Scope of This SAS

1. This Statement on Auditing Standards (SAS) addresses the auditor’s responsibility to

identify and assess the risks of material misstatement in the financial statements.

Key Concepts in This SAS

2. AU-C section 200, Overall Objectives of the Independent Auditor and the Conduct of an

Audit in Accordance With Generally Accepted Auditing Standards, addresses the overall objectives

of the auditor in conducting an audit of the financial statements, including to obtain sufficient

appropriate audit evidence to reduce audit risk to an acceptably low level.

1

Audit risk is a function

of the risks of material misstatement and detection risk.

2

AU-C section 200 explains that the risks

of material misstatement may exist at two levels:

3

the overall financial statement level and the

assertion level for classes of transactions, account balances, and disclosures.

3. AU-C section 200 requires the auditor to exercise professional judgment in planning and

performing an audit and to plan and perform an audit with professional skepticism, recognizing

that circumstances may exist that cause the financial statements to be materially misstated.

4

4. Risks at the financial statement level relate pervasively to the financial statements as a

whole and potentially affect many assertions. Risks of material misstatement at the assertion level

consist of two components:

5

inherent risk and control risk.

• Inherent risk is described as the susceptibility of an assertion about a class of

transactions, account balance, or disclosure to a misstatement that could be material,

either individually or when aggregated with other misstatements, before consideration

of any related controls.

• Control risk is described as the risk that a misstatement that could occur in an

assertion about a class of transactions, account balance, or disclosure and that could

1

Paragraph .19 of AU-C section 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit

in Accordance With Generally Accepted Auditing Standards.

2

Paragraph .14 of AU-C section 200.

3

Paragraph .A38 of AU-C section 200.

4

Paragraphs .17–.18 of AU-C section 200.

5

Paragraph .14 of AU-C section 200.

be material, either individually or when aggregated with other misstatements, will not

be prevented, or detected and corrected, on a timely basis by the entity’s system of

internal control.

5. AU-C section 200 explains that risks of material misstatement are assessed at the assertion

level in order to determine the nature, timing, and extent of further audit procedures necessary to

obtain sufficient appropriate audit evidence. For purposes of generally accepted auditing standards

(GAAS), a risk of material misstatement exists when (a) there is a reasonable possibility of a

misstatement occurring (that is, its likelihood), and (b) if it were to occur, there is a reasonable

possibility of the misstatement being material (that is, its magnitude).

6

For the identified risks of

material misstatement at the assertion level, a separate assessment of inherent risk and control risk

is required by this SAS. As explained in AU-C section 200, inherent risk is higher for some

assertions and related classes of transactions, account balances, and disclosures than for others.

The degree to which the level of inherent risk varies is referred to in this SAS as the spectrum of

inherent risk.

6. Risks of material misstatement identified and assessed by the auditor include both those

due to error and those due to fraud. Although both are addressed by this SAS, the significance of

fraud is such that further requirements and guidance are included in AU-C section 240,

Consideration of Fraud in a Financial Statement Audit, in relation to risk assessment procedures

and related activities to obtain information that is used to identify, assess, and respond to the risks

of material misstatement due to fraud.

7. The auditor’s risk identification and assessment process is iterative and dynamic. The

auditor’s understanding of the entity and its environment, the applicable financial reporting

framework, and the entity’s system of internal control are interdependent with concepts within the

requirements to identify and assess the risks of material misstatement. In obtaining the

understanding required by this SAS, initial expectations of risks may be developed, which may be

further refined as the auditor progresses through the risk identification and assessment process. In

addition, paragraph 41 of this SAS and AU-C section 330, Performing Audit Procedures in

Response to Assessed Risks and Evaluating the Audit Evidence Obtained,

7

require the auditor to

revise the risk assessments and modify further overall responses and further audit procedures,

based on audit evidence obtained from performing further audit procedures in accordance with

AU-C section 330, or if new information is obtained.

8. AU-C section 330 requires the auditor to design and implement overall responses to address

the assessed risks of material misstatement at the financial statement level.

8

AU-C section 330

further explains that the auditor’s assessment of the risks of material misstatement at the financial

statement level, and the auditor’s overall responses, is affected by the auditor’s understanding of

the control environment. AU-C section 330 also requires the auditor to design and perform further

audit procedures whose nature, timing, and extent are based on and are responsive to the assessed

6

Paragraph .A41‒.A43 of AU-C section 200 and paragraph .07 of AU-C section 330, Performing Audit Procedures

in Response to Assessed Risks and Evaluating the Audit Evidence Obtained.

7

Paragraph .27 of AU-C section 330.

8

Paragraph .05 of AU-C section 330.

risks of material misstatement at the relevant assertion level.

9

Scalability

9. AU-C section 200 states that some AU-C sections include scalability considerations, which

illustrate the application of the requirements to all entities, regardless of whether their nature and

circumstances are less complex or more complex.

10

This SAS is intended for audits of all entities,

regardless of size or complexity; therefore, the application material incorporates considerations

specific to both less and more complex entities, where appropriate. Although the size of an entity

may be an indicator of its complexity, some smaller entities may be complex, and some larger

entities may be less complex.

Effective Date

10. This SAS is effective for audits of financial statements for periods ending on or after

December 15, 2023.

Objective

11. The objective of the auditor is to identify and assess the risks of material misstatement,

whether due to fraud or error, at the financial statement and assertion levels, thereby providing a

basis for designing and implementing responses to the assessed risks of material misstatement.

Definitions

12. For purposes of GAAS, the following terms have the meanings attributed:

Assertions. Representations, explicit or otherwise, with respect to the recognition,

measurement, presentation, and disclosure of information in the financial

statements, which are inherent in management, representing that the financial

statements are prepared in accordance with the applicable financial reporting

framework. Assertions are used by the auditor to consider the different types of

potential misstatements that may occur when identifying, assessing, and responding

to the risks of material misstatement. (Ref: par. A1)

Business risk. A risk resulting from significant conditions, events, circumstances,

actions, or inactions that could adversely affect an entity’s ability to achieve its

objectives and execute its strategies, or from the setting of inappropriate objectives

and strategies.

9

Paragraph .06 of AU-C section 330.

10

Paragraph .A68 of AU-C section 200.

Controls. Policies or procedures that an entity establishes to achieve the control

objectives of management or those charged with governance. In this context (Ref:

par. A2–A5)

i. policies are statements of what should, or should not, be done within the entity

to effect control. Such statements may be documented, explicitly stated in

communications, or implied through actions and decisions.

ii. procedures are actions to implement policies.

General information technology (IT) controls. Controls over the entity’s IT processes

that support the continued proper operation of the IT environment, including the

continued effective functioning of information-processing controls and the integrity

of information in the entity’s information system. Also see IT environment. (Ref:

par. A6)

Information-processing controls. Controls relating to the processing of information in

IT applications or manual information processes in the entity’s information system

that directly address risks to the integrity of information. (Ref: par. A7–A8)

Inherent risk factors. Characteristics of events or conditions that affect the

susceptibility to misstatement, whether due to fraud or error, of an assertion about a

class of transactions, account balance, or disclosure, before consideration of

controls. Such factors may be qualitative or quantitative and include complexity,

subjectivity, change, uncertainty, or susceptibility to misstatement due to

management bias or other fraud risk factors

11

insofar as they affect inherent risk.

Depending on the degree to which the inherent risk factors affect the susceptibility

of an assertion to misstatement, the level of inherent risk varies on a scale that is

referred to as the spectrum of inherent risk. (Ref: par. A9–A11, A238–A244)

IT environment. The IT applications and supporting IT infrastructure, as well as the IT

processes and personnel involved in those processes, that an entity uses to support

business operations and achieve business strategies. For the purposes of this

definition

i. an IT application is a program or a set of programs that is used in the initiation,

processing, recording, and reporting of transactions or information. IT

applications include data warehouses and report writers.

ii. the IT infrastructure comprises the network, operating systems, and databases

and their related hardware and software.

11

Paragraphs .A28‒.A32 of AU-C section 240, Consideration of Fraud in a Financial Statement Audit.

iii. the IT processes are the entity’s processes to manage access to the IT

environment, manage program changes or changes to the IT environment, and

manage IT operations.

Relevant assertions. An assertion about a class of transactions, account balance, or

disclosure is relevant when it has an identified risk of material misstatement. A risk

of material misstatement exists when (a) there is a reasonable possibility of a

misstatement occurring (that is, its likelihood), and (b) if it were to occur, there is a

reasonable possibility of the misstatement being material (that is, its magnitude).

12

The determination of whether an assertion is a relevant assertion is made before

consideration of any related controls (that is, the determination is based on inherent

risk). (Ref: par. A12)

Risks arising from the use of IT. Susceptibility of information-processing controls to

ineffective design or operation, or risks to the integrity of information in the entity’s

information system, due to ineffective design or operation of controls in the entity’s

IT processes. See IT environment. (Ref: par. A6 and A13)

Risk assessment procedures. The audit procedures designed and performed to identify

and assess the risks of material misstatement, whether due to fraud or error, at the

financial statement and assertion levels.

Significant class of transactions, account balance, or disclosure. A class of

transactions, account balance, or disclosure for which there is one or more relevant

assertions. (Ref: par. A14)

Significant risk. An identified risk of material misstatement (Ref: par. A15)

i. for which the assessment of inherent risk is close to the upper end of the spectrum

of inherent risk due to the degree to which inherent risk factors affect the

combination of the likelihood of a misstatement occurring and the magnitude of

the potential misstatement should that misstatement occur, or

ii. that is to be treated as a significant risk in accordance with the requirements of

other AU-C sections.

13

System of internal control. The system designed, implemented, and maintained by those

charged with governance, management, and other personnel to provide reasonable

assurance about the achievement of an entity’s objectives with regard to reliability of

financial reporting, effectiveness and efficiency of operations, and compliance with

12

Paragraphs .A41‒.A43 of AU-C section 200 and paragraph .07 of AU-C section 330.

13

Paragraph .27 of AU-C section 240 and paragraph .20 of AU-C section 550, Related Parties.

applicable laws and regulations. For purposes of GAAS, the system of internal control

consists of five interrelated components:

i. Control environment

ii. The entity’s risk assessment process

iii. The entity’s process to monitor the system of internal control

iv. The information system and communication

v. Control activities

(Ref: par. A16)

Requirements

Risk Assessment Procedures and Related Activities

13. The auditor should design and perform risk assessment procedures to obtain audit evidence

that provides an appropriate basis for (Ref: par. A17–A24)

a. the identification and assessment of risks of material misstatement, whether due to

fraud or error, at the financial statement and assertion levels, and

b. the design of further audit procedures in accordance with AU-C section 330.

The auditor should design and perform risk assessment procedures in a manner that is not biased

towards obtaining audit evidence that may be corroborative or towards excluding audit evidence

that may be contradictory.

14. The risk assessment procedures should include the following: (Ref: par. A25–A27)

a. Inquiries of management and of other appropriate individuals within the entity,

including individuals within the internal audit function (if the function exists) (Ref: par.

A28–A32)

b. Analytical procedures (Ref: par. A33–A37)

c. Observation and inspection (Ref: par. A38–A42)

Information From Other Sources

15. In obtaining audit evidence in accordance with paragraph 13, the auditor should consider

information from (Ref: par. A43‒A44)

a. the auditor’s procedures regarding acceptance or continuance of the client relationship

or the audit engagement, and

b. when applicable, other engagements performed by the engagement partner for the

entity.

16. When the auditor intends to use information obtained from the auditor’s previous

experience with the entity and from audit procedures performed in previous audits, the auditor

should evaluate whether such information remains relevant and reliable as audit evidence for the

current audit. (Ref: par. A45‒A47)

Engagement Team Discussion

17. The engagement partner and other key engagement team members should discuss the

application of the applicable financial reporting framework and the susceptibility of the entity’s

financial statements to material misstatement. (Ref: par. A48–A54)

18. When there are engagement team members not involved in the engagement team

discussion, the engagement partner should determine which matters are to be communicated to

those members.

Obtaining an Understanding of the Entity and Its Environment, the Applicable Financial

Reporting Framework, and the Entity’s System of Internal Control (Ref: par. A55‒A57)

Understanding the Entity and Its Environment, and the Applicable Financial Reporting

Framework (Ref: par. A58‒A63)

19. The auditor should perform risk assessment procedures to obtain an understanding of

a. the following aspects of the entity and its environment:

i. The entity’s organizational structure, ownership and governance, and its business

model, including the extent to which the business model integrates the use of IT

(Ref: par. A64‒A77)

ii. Industry, regulatory, and other external factors (Ref: par. A78‒A82)

iii. The measures used, internally and externally, to assess the entity’s financial

performance (Ref: par. A83‒A90)

b. the applicable financial reporting framework and the entity’s accounting policies and

the reasons for any changes thereto. (Ref: par. A91‒A93)

c. how inherent risk factors affect the susceptibility of assertions to misstatement and the

degree to which they do so, in the preparation of the financial statements in accordance

with the applicable financial reporting framework, based on the understanding obtained

in subparagraphs a−b. (Ref: par. A94‒A99)

20. The auditor should evaluate whether the entity’s accounting policies are appropriate and

consistent with the applicable financial reporting framework.

Understanding the Components of the Entity’s System of Internal Control (Ref: par. A100–

A111)

Control Environment, the Entity’s Risk Assessment Process, and the Entity’s Process to Monitor

the System of Internal Control (Ref: par. A112‒A114)

Control Environment

21. The auditor should, through performing risk assessment procedures, obtain an

understanding of the control environment relevant to the preparation of the financial statements by

(Ref: par. A115–A116)

a. understanding the set of controls, processes, and structures that address (Ref: par.

A117)

i. how management’s oversight responsibilities are carried out, such as the entity’s

culture and management’s commitment to integrity and ethical values;

ii. when those charged with governance are separate from management, the

independence of, and oversight over the entity’s system of internal control by, those

charged with governance;

iii. the entity’s assignment of authority and responsibility;

iv. how the entity attracts, develops, and retains competent individuals;

v. how the entity holds individuals accountable for their responsibilities in the pursuit

of the objectives of the system of internal control; and

b. evaluating, based on the auditor’s understanding obtained in paragraph 21a, whether

(Ref: par. A118‒A123)

i. management, with the oversight of those charged with governance, has created and

maintained a culture of honesty and ethical behavior;

ii. the control environment provides an appropriate foundation for the other

components of the entity’s system of internal control considering the nature and

complexity of the entity; and

iii. control deficiencies identified in the control environment undermine the other

components of the entity’s system of internal control

The Entity’s Risk Assessment Process

22. The auditor should, through performing risk assessment procedures, obtain an

understanding of the entity’s risk assessment process relevant to the preparation of the financial

statements by

a. understanding the entity’s process for (Ref: par. A124‒A126)

i. identifying business risks, including the potential for fraud, relevant to financial

reporting objectives; (Ref: par. A71)

ii. assessing the significance of those risks, including the likelihood of their

occurrence;

iii. addressing those risks; and

b. evaluating, based on the auditor’s understanding obtained in paragraph 22a, whether

the entity’s risk assessment process is appropriate to the entity’s circumstances

considering the nature and complexity of the entity. (Ref: par. A127‒A129)

23. If the auditor identifies risks of material misstatement that management failed to identify,

the auditor should

a. determine whether any such risks are of a kind that the auditor expects would have been

identified by the entity’s risk assessment process and, if so, obtain an understanding of

why the entity’s risk assessment process failed to identify such risks of material

misstatement; and

b. consider the implications for the auditor’s evaluation in paragraph 22b.

The Entity’s Process for Monitoring the System of Internal Control

24. The auditor should, through performing risk assessment procedures, obtain an

understanding of the entity’s process for monitoring the system of internal control relevant to the

preparation of the financial statements by (Ref: par. A130–A131)

a. understanding those aspects of the entity’s process that address

i. ongoing and separate evaluations for monitoring the effectiveness of controls and

the identification and remediation of control deficiencies identified (Ref: par.

A132‒A133) and

ii. the entity’s internal audit function, if any, including its nature, responsibilities, and

activities (Ref: par. A134‒A135).

b. understanding the sources of the information used in the entity’s process to monitor the

system of internal control, and the basis upon which management considers the

information to be sufficiently reliable for the purpose (Ref: par. A136‒A137).

c. evaluating, based on the auditor’s understanding obtained in paragraph 24a–b, whether

the entity’s process for monitoring the system of internal control is appropriate to the

entity’s circumstances considering the nature and complexity of the entity (Ref: par.

A138‒A139).

Information System and Communication, and Control Activities (Ref: par. A140–A147)

The Information System and Communication

25. The auditor should, through performing risk assessment procedures, obtain an

understanding of the entity’s information system and communication relevant to the preparation

of the financial statements by (Ref: par. A148–A149)

a. understanding the entity’s information-processing activities, including its data and

information, the resources to be used in such activities and the policies that define, for

significant classes of transactions, account balances, and disclosures (Ref: par. A150‒

A162)

i. how information flows through the entity’s information system, including how

(1) transactions are initiated, and how information about them is recorded,

processed, corrected as necessary, incorporated in the general ledger, and

reported in the financial statements and

(2) information about events and conditions, other than transactions, is captured,

processed, and disclosed in the financial statements,

ii. the accounting records, specific accounts in the financial statements, and other

supporting records relating to the flows of information in the information system,

iii. the financial reporting process used to prepare the entity’s financial statements,

including disclosures, and

iv. the entity’s resources, including the IT environment, relevant to preceding a(i)–

(iii).

b. understanding how the entity communicates significant matters that support the

preparation of the financial statements and related reporting responsibilities in the

information system and other components of the system of internal control (Ref: par.

A163‒A164)

i. between people within the entity, including how financial reporting roles and

responsibilities are communicated,

ii. between management and those charged with governance,

iii. with external parties, such as those with regulatory authorities.

c. evaluating, based on the auditor’s understanding obtained in paragraph 25a–b, whether

the entity’s information system and communication appropriately support the

preparation of the entity’s financial statements in accordance with the applicable

financial reporting framework considering the nature and complexity of the entity.

(Ref: par. A165).

Control Activities

26. The auditor should, through performing risk assessment procedures, obtain an

understanding of the control activities component, by applying the requirements in paragraphs 27–

30. (Ref: par. A167–A179)

27. The auditor should identify the following controls that address risks of material

misstatement at the assertion level:

a. Controls that address a risk that is determined to be a significant risk (Ref: par. A180‒

A181)

b. Controls over journal entries and other adjustments as required by AU-C section 240

14

(Ref: par. A182‒A183)

c. Controls for which the auditor plans to test operating effectiveness in determining the

nature, timing, and extent of substantive procedures, which should include controls that

address risks for which substantive procedures alone do not provide sufficient

appropriate audit evidence (Ref: par. A184‒A186)

d. Other controls that, based on the auditor’s professional judgment, the auditor considers

are appropriate to enable the auditor to meet the objectives of paragraph 13 with respect

to risks at the assertion level (Ref: par. A187‒A188)

28. Based on controls identified in paragraph 27, the auditor should identify the IT applications

and the other aspects of the entity’s IT environment that are subject to risks arising from the use

of IT.

29. For the IT applications and other aspects of the IT environment identified in paragraph 28,

the auditor should identify the following: (Ref: par. A189‒A200)

a. The related risks arising from the use of IT

b. The entity’s general IT controls that address such risks

30. For each control identified in paragraph 27 or 29b, the auditor should (Ref: par. A201‒

A210)

a. evaluate whether the control is designed effectively to address the risk of material

misstatement at the assertion level or effectively designed to support the operation of

other controls.

b. determine whether the control has been implemented by performing procedures in

addition to inquiry of the entity’s personnel.

Control Deficiencies Within the Entity’s System of Internal Control

31. Based on the auditor’s understanding and evaluation of the components of the entity’s

system of internal control as required by this SAS, the auditor should determine whether one or

more control deficiencies have been identified. (Ref: par. A211–A212)

Identifying and Assessing the Risks of Material Misstatement (Ref: par. A213–A214)

Identifying Risks of Material Misstatement

14

Paragraph 32a(i) of AU-C section 240.

32. The auditor should identify the risks of material misstatement and determine whether they

exist at (Ref: par. A215–A221)

a. the financial statement level (Ref: par. A222–A229) or

b. the assertion level for classes of transactions, account balances, and disclosures (Ref:

par. A230–A231).

33. The auditor should determine the relevant assertions and the related significant classes of

transactions, account balances, and disclosures. (Ref: par. A232–A234)

Assessing Risks of Material Misstatement at the Financial Statement Level

34. For identified risks of material misstatement at the financial statement level, the auditor

should assess the risks and (Ref: par. A222–A229)

a. determine whether such risks affect the assessment of risks at the assertion level, and

b. evaluate the nature and extent of their pervasive effect on the financial statements.

Assessing Risks of Material Misstatement at the Assertion Level

Assessing Inherent Risk (Ref: par. A235–A244)

35. For identified risks of material misstatement at the assertion level, the auditor should assess

inherent risk by assessing the likelihood and magnitude of misstatement. In doing so, the auditor

should take into account how, and the degree to which

a. inherent risk factors affect the susceptibility of relevant assertions to misstatement, and

b. the risks of material misstatement at the financial statement level affect the assessment

of inherent risk for risks of material misstatement at the assertion level. (Ref: par.

A245–A246)

36. The auditor should determine whether any of the assessed risks of material misstatement

are significant risks. (Ref: par. A247–A251)

37. The auditor should determine whether substantive procedures alone cannot provide

sufficient appropriate audit evidence for any of the risks of material misstatement at the assertion

level. (Ref: par. A252–A255)

Assessing Control Risk

38. For identified risks of material misstatement at the assertion level, the auditor should assess

control risk based on the auditor’s understanding of controls and the auditor’s plan to test the

operating effectiveness of controls. If the auditor does not plan to test the operating effectiveness

of controls, the auditor should assess control risk at the maximum level such that the assessment

of the risk of material misstatement is the same as the assessment of inherent risk. (Ref: par. A256–

A260)

Evaluating the Audit Evidence Obtained From the Risk Assessment Procedures

39. The auditor should evaluate whether the audit evidence obtained from the risk assessment

procedures provides an appropriate basis for the identification and assessment of the risks of

material misstatement. If not, the auditor should perform additional risk assessment procedures

until audit evidence has been obtained to provide such a basis. In identifying and assessing the

risks of material misstatement, the auditor should take into account all audit evidence obtained

from the risk assessment procedures, whether corroborative or contradictory to assertions made by

management. (Ref: par. A261–A263)

Classes of Transactions, Account Balances, and Disclosures That Are Not Significant but

Are Material

40. For material classes of transactions, account balances, or disclosures that have not been

determined to be significant classes of transactions, account balances, or disclosures, the auditor

should evaluate whether the auditor’s determination remains appropriate. (Ref: par. A264–A265)

Revision of Risk Assessment

41. If the auditor obtains new information that is inconsistent with the audit evidence on which

the auditor originally based the identification or assessments of the risks of material misstatement,

the auditor should revise the identification or assessment. (Ref: par. A266)

Documentation

42. The auditor should include in the audit documentation

15

(Ref: par. A267–A273)

a. the discussion among the engagement team in accordance with paragraphs 17 and 18

and the significant decisions reached;

b. key elements of the auditor’s understanding in accordance with paragraphs 19, 21, 22,

24, and 25; the sources of information from which the auditor’s understanding was

obtained; and the risk assessment procedures performed;

c. the evaluation of the design of identified controls, and determination whether such

controls have been implemented, in accordance with paragraph 30; and

d. the identified and assessed risks of material misstatement at the financial statement

level and at the assertion level, including significant risks and risks for which

substantive procedures alone cannot provide sufficient appropriate audit evidence, and

the rationale for the significant judgments made.

***

Application and Other Explanatory Material

15

Paragraphs .08–.12 and .A8–.A9 of AU-C section 230, Audit Documentation.

Definitions (Ref: par. 12)

Assertions

A1. Categories of assertions are used by auditors to consider the different types of potential

misstatements that may occur when identifying, assessing, and responding to the risks of material

misstatement. Examples of these categories of assertions are described in paragraph A219. The

assertions differ from the written representations required by AU-C section 580, Written

Representations, to confirm certain matters or support other audit evidence.

Controls

A2. Controls are embedded within the components of the entity’s system of internal control.

A3. Policies are implemented through the actions of personnel within the entity or through the

restraint of personnel from taking actions that would conflict with such policies.

A4. Procedures may be mandated, through formal documentation or other communication by

management or those charged with governance, or may result from behaviors that are not mandated

but, rather, are conditioned by the entity’s culture. Procedures may be enforced through the actions

permitted by the IT applications used by the entity or other aspects of the entity’s IT environment.

A5. Controls may be direct or indirect (see paragraphs A112, A140, and A168). Direct controls

are controls that are precise enough to address risks of material misstatement at the assertion level.

Indirect controls are controls that support direct controls. Although indirect controls are not

sufficiently precise to prevent, or detect and correct, misstatements at the assertion level, they are

foundational and may have an indirect effect on the likelihood that a misstatement will be

prevented or detected on a timely basis.

General IT Controls

A6. The integrity of information may include the completeness, accuracy, and validity of

transactions and other information. Although this SAS does not prescribe the use of a particular

internal control framework, the auditor may find the following guidance regarding the concepts

encompassed by the term validity, from COSO’s 2013 Internal Control—Integrated Framework

(COSO framework), helpful: “Recorded transactions represent economic events that actually

occurred and were executed according to prescribed procedures. Validity is generally achieved

through control activities that include the authorization of transactions as specified by an